An interest rate increase of 0.5% will increase the monthly repayment of mortgage holders by an additional 100 shekels, completing an increase of approximately one thousand shekels within a year. of insolvency

The Monetary Committee of the Bank of Israel decided today on another interest rate increase – for the eighth time in a row to a level of 4.25% . What does it mean for the hundreds of thousands of mortgage takers or in general those who took out a loan linked to the prime interest rate (Bank of Israel interest plus 1.5%)?

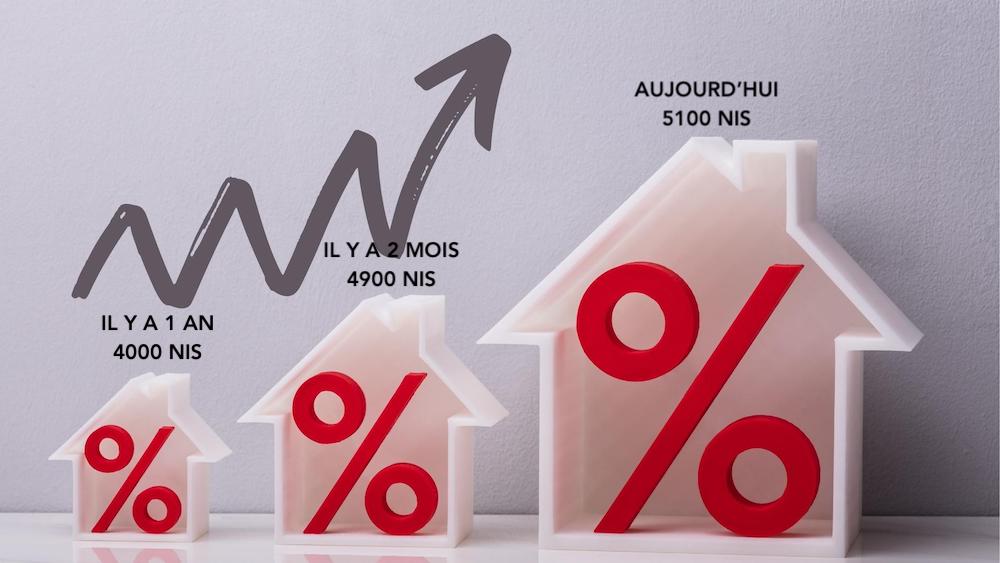

According to a simulation conducted by Vader Mortgages for Globes, based on an average mortgage of one million shekels divided into 35% in the prime route, 40% in fixed interest (not linked) and 25% in variable interest (linked), today’s interest rate increase of 0.5% resulted in that the monthly repayment over the 30 years of her mortgage crossed the threshold of NIS 5,000. This is an addition of another NIS 100 to the monthly repayment compared to today, on the same loan vehicle. This after in just one year, the public’s monthly repayment jumped by about a thousand shekels, mainly after the prime interest rate jumped threefold.

When you add to the jump in mortgage repayments the continued increase in the cost of living, the fear is that the mortgage-taking public will not be able to meet the repayments. Indeed, the banks do recognize an increase in the volume of requests to freeze the monthly payment, for periods of time of several months. This is an increase from a few tens to hundreds (at the low bar). True, we are not talking about the tens of thousands who requested a moratorium on mortgages with the outbreak of the corona virus, but the banks are following the trend.

Banks conduct business as usual

In general, the banks do not convey real concern about not meeting the mortgage repayments. “When the culture in Israel is that a person needs to own an apartment, he will still be in the market for apartment buyers and will not give up the apartment if he already owns one,” says a senior banking official. “Every increase in the interest rate affects the margins of the loan takers, who are more sensitive, because there is no such thing as an increase in interest does not affect, but I assume that we will not see a dramatic change among those who took out mortgages. If there is a certain risk in the market, it does not come from customers who have already taken out a mortgage, But with those who are now asking for a mortgage after housing prices jumped by 20%. This means that a property worth NIS 2 million has become more expensive by NIS 400,000, and in order to finance the equity, a young couple needs to raise NIS 500,000 to get a loan.”